Portfolio rebalancing involves more than shifting assets—it’s a strategic process. From setting target allocations to deciding when to rebalance, understanding the methodology ensures that your portfolio remains on track for growth.

Portfolio rebalancing involves more than shifting assets—it’s a strategic process. From setting target allocations to deciding when to rebalance, understanding the methodology ensures that your portfolio remains on track for growth.

Those seeking guidance on rebalancing techniques can connect with experts through the investment firms for tailored insights.

Calendar-Based vs. Threshold-Based Rebalancing Strategies

There are two common methods for rebalancing: calendar-based and threshold-based. The calendar-based method is straightforward. It’s like setting a recurring reminder to water your plants.

You choose specific dates—monthly, quarterly, or annually—and check your portfolio to see if it needs adjustments. This approach keeps things simple and regular, making it easy to stay on top of rebalancing.

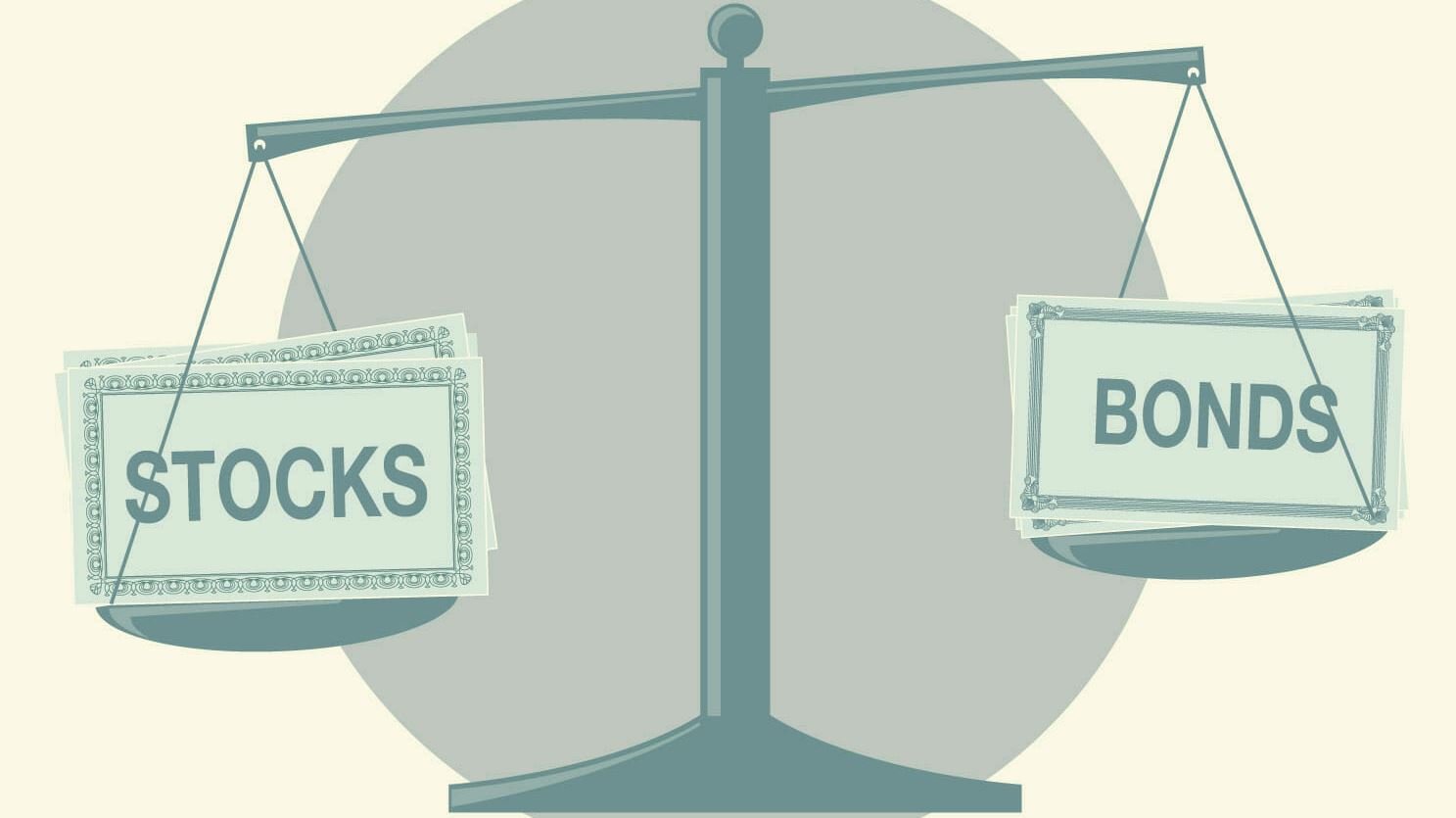

On the other hand, threshold-based rebalancing focuses on your asset allocation. With this strategy, you only rebalance when one asset class strays too far from its original percentage in your portfolio.

Picture a scale that tips over when one side gets too heavy—this method keeps your investments balanced. If your portfolio was set up to be 60% stocks and 40% bonds, and stocks grow to 70%, you would rebalance to get back to your target allocation.

This strategy responds to actual market conditions instead of a fixed schedule, potentially saving you from unnecessary trades and fees.

While calendar-based rebalancing is easier to implement, it might not be as responsive to market shifts. In contrast, threshold-based rebalancing requires more monitoring, but it’s likely to keep your portfolio closer to its intended risk level.

Both methods have their strengths, so the choice comes down to how hands-on you want to be. What works best for you—routine check-ins or responding only when your portfolio goes off track?

Automated vs. Manual Rebalancing: Pros and Cons

Automated rebalancing has gained popularity thanks to the rise of robo-advisors. With this method, a computer takes care of everything. Once your preferences are set, the system automatically adjusts your portfolio as needed. It’s like having a self-driving car for your investments—you can sit back and relax.

One major benefit is convenience. You don’t need to constantly watch your portfolio or worry about making emotional decisions during market swings.

However, some investors prefer manual rebalancing. They want more control over when and how adjustments are made. Think of it as driving your own car—you choose the route and speed.

Manual rebalancing lets you make decisions based on personal preferences or market insights, something an algorithm can’t do as well. You can choose the exact moment to buy or sell, potentially allowing for more strategic moves.

Of course, manual rebalancing requires time and effort. You’ll need to regularly check your portfolio and make decisions, which can be challenging for those who aren’t well-versed in the markets.

On the flip side, automation removes this burden but might not always optimize for the best possible outcome.

Automated systems stick strictly to rules, which might not always align with your financial goals as situations change. So, which would you rather have—a set-and-forget system or hands-on control?

Rebalancing Frequency: Finding the Optimal Schedule

How often should you rebalance your portfolio? It’s a bit like deciding how frequently to get your car serviced—not too often, but not too rarely either. The right frequency depends on a few factors, like your risk tolerance, market conditions, and the type of assets in your portfolio.

If you rebalance too often, you might incur more transaction fees than necessary.

Every time you buy or sell assets, you’re likely to face some costs, and frequent trades can chip away at your returns over time. Also, markets can be unpredictable in the short term, so constantly adjusting your portfolio might lead you to chase market movements—something most experts recommend avoiding.

On the other hand, if you wait too long to rebalance, your portfolio could drift far from its original allocation.

It’s like waiting too long to take your car in for maintenance—you might find yourself dealing with bigger issues later. A portfolio that’s too out of balance might expose you to more risk than you’re comfortable with.

Most experts suggest rebalancing once or twice a year as a general rule of thumb. However, this isn’t set in stone. You might adjust the frequency depending on how much market volatility you’re experiencing or if your life circumstances have changed.

At the end of the day, the best schedule is one that fits your goals without overcomplicating your strategy. Does your current rebalancing routine feel right, or is it time for an adjustment?

Conclusion

The methodology of portfolio rebalancing is essential for long-term success. By following structured steps, investors can keep their portfolios balanced, aligned with goals, and primed for sustainable growth.